Market Risk vs Portfolio Risk: A Simple Comparison in Investment Research

October 21, 2025 | By GenRPT Finance

Market risk and portfolio risk are closely related, but they measure different aspects of investment uncertainty. Market risk refers to the possibility that broad economic or financial events will affect the overall market, while portfolio risk measures the risk associated with the specific mix of investments held in a portfolio. Understanding the difference helps investors identify which risks are unavoidable and which can be managed through diversification and portfolio construction.

Every investment carries risk.

However, not every risk originates from the same source.

A company’s earnings may decline because of poor management decisions, while an entire market may fall because of rising interest rates or geopolitical tensions.

Professional equity research separates these risks to provide investors with a clearer understanding of where uncertainty comes from and how it can be managed.

According to the CFA Institute, effective portfolio management depends on understanding both systematic and portfolio-specific risks rather than focusing only on individual stock performance. This distinction helps investment professionals make more balanced allocation decisions while improving long-term returns.

What Is Market Risk?

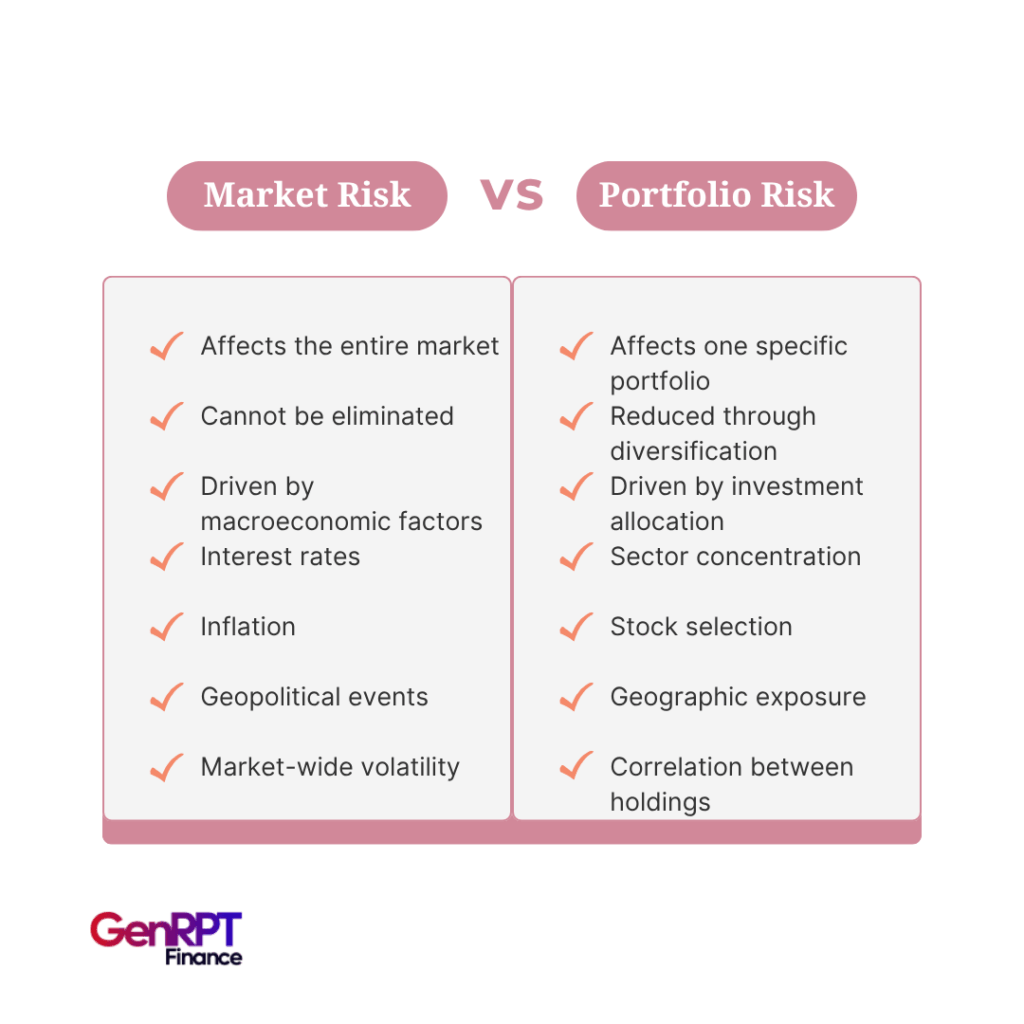

Market risk refers to the possibility that external events will affect the value of investments across the broader market.

These events are largely beyond the control of individual companies.

Common sources of market risk include:

- Interest rate changes

- Inflation

- Economic recessions

- Currency movements

- Geopolitical factors

- Government policy changes

- Commodity price fluctuations

For example, when central banks increase interest rates, stock markets across multiple sectors may experience lower valuations even if individual companies continue performing well.

Because market risk affects nearly every investor, it cannot be eliminated completely through diversification.

It forms an important part of market risk analysis within investment research.

What Is Portfolio Risk?

It measures the uncertainty associated with a specific collection of investments.

Unlike market risk, portfolio risk depends largely on investment decisions.

Factors influencing portfolio risk analysis include:

- Sector concentration

- Geographic exposure

- Asset allocation

- Stock selection

- Currency exposure

- Position sizing

- Correlation between holdings

For example, a portfolio invested entirely in technology companies carries higher concentration risk than one diversified across healthcare, financial services, manufacturing, and consumer goods.

Portfolio risk can often be reduced through diversification and disciplined portfolio construction.

Market Risk Affects Everyone

Market risk is considered systematic.

It influences nearly all companies operating within financial markets.

Examples include:

During the COVID-19 pandemic, markets worldwide experienced significant declines regardless of individual company performance.

Similarly, rising inflation and interest rates affected technology valuations across global equity markets.

Even companies with strong fundamentals experienced lower valuations because investor expectations changed across the broader market.

This demonstrates why analysts continuously monitor the macroeconomic outlook, inflation, interest rates, and market trends.

Portfolio Risk Is Unique to Every Investor

Two investors can own completely different portfolios while operating within the same market.

One portfolio may emphasize technology and growth stocks.

Another may focus on dividend-paying industrial companies.

Although both investors face identical market conditions, their portfolio risks differ significantly.

Analysts evaluate:

- Diversification

- Individual company exposure

- Industry allocation

- Geographic diversification

- Investment objectives

These factors determine how sensitive a portfolio is to different market events.

How Analysts Measure Market Risk

Professional analysts evaluate market risk using both economic and financial indicators.

Common measures include:

- Interest rate trends

- Inflation expectations

- Market volatility

- Economic growth

- Currency movements

- Commodity prices

- Global political developments

These indicators influence financial forecasting, Scenario Analysis, and long-term Equity Valuation.

How Analysts Measure Portfolio Risk

Portfolio risk focuses on the investments themselves.

Analysts evaluate:

- Portfolio diversification

- Correlation between holdings

- Position concentration

- Sector exposure

- Company-specific risks

- Equity risk

- Liquidity analysis

Rather than asking how markets might perform, analysts evaluate how individual holdings interact with one another.

This strengthens risk assessment and supports better capital allocation.

Why Both Risks Matter Together

Market risk and portfolio risk should never be evaluated independently.

A diversified portfolio may still perform poorly during severe market downturns.

Likewise, strong market conditions cannot compensate for a poorly diversified portfolio.

Professional investors combine:

- Market risk analysis

- Portfolio risk analysis

- Company fundamentals

- Business quality

- Competitive intelligence

This integrated approach creates more balanced investment decisions.

AI Is Improving Risk Analysis

Modern investment research requires monitoring thousands of data points.

Analysts review:

- Financial reports

- Earnings calls

- Economic indicators

- Market news

- Regulatory developments

- Portfolio exposures

Using ai for equity research, research platforms continuously monitor both market-wide developments and portfolio-level risks.

With ai data analysis, AI identifies changing market conditions, highlights concentration risks, and generates structured equity research reports that combine company analysis with portfolio insights.

This allows investment professionals to respond more quickly to changing market conditions.

Conclusion

Understanding the difference between market risk and portfolio risk helps investors make better-informed decisions. While market risk reflects broad economic and financial conditions that influence all investments, portfolio risk depends on how individual assets are selected and combined. Evaluating both together enables analysts to build stronger portfolios, improve diversification, and develop more realistic investment strategies.

GenRPT Finance simplifies both market risk analysis and portfolio risk analysis by combining financial statements, macroeconomic data, earnings calls, regulatory filings, market intelligence, and AI-powered analytics into comprehensive research reports. Powered by Yodaplus Agentic AI services, the platform helps investment professionals monitor changing risks, strengthen portfolio construction, and generate deeper investment insights with greater speed and consistency.

FAQs

Market risk affects the entire financial market because of external economic factors, while portfolio risk depends on the composition and diversification of a specific investment portfolio.

No. Market risk is systematic and cannot be completely eliminated, although investors can manage its impact through asset allocation and risk management strategies.

Yes. Portfolio risk can often be reduced through diversification, balanced asset allocation, and careful investment selection.

Evaluating both provides a more complete understanding of investment uncertainty, helping investors distinguish between broad market events and portfolio-specific vulnerabilities.

AI continuously analyzes financial reports, market data, macroeconomic indicators, portfolio exposures, and news to identify changing risks and generate actionable investment insights.

GenRPT Finance combines AI-powered financial analysis, macroeconomic intelligence, portfolio analytics, and market monitoring to help investment professionals evaluate market and portfolio risks more efficiently.